- Dollar pauses slide as jobs and inflation data awaited

- Yen pulls back but hawkish BoJ signals keep it elevated

- Wall Street awaits Nvidia, oil retreats on demand worries

Dollar awaits key data for direction

The US dollar extended its slump against all its major peers on Tuesday, as in the absence of any top-tier data and shocking headlines, investors continued to digest Powell’s dovish stance at Jackson Hole.

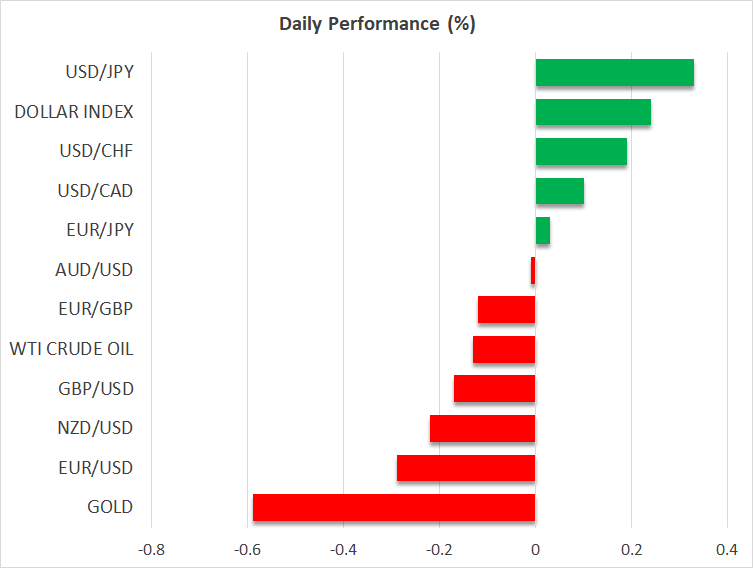

However, today, the dollar is in a recovery mode, perhaps as short sellers are liquidating their positions ahead of important releases tomorrow and Friday. Bearing in mind that Powell stressed the importance of the labor market, tomorrow’s initial jobless claims may attract more attention than usual, while on Friday, the core PCE price index, the Fed’s favorite inflation gauge, is due to be released.

Following Powell’s remarks, more market participants were convinced that the Fed may proceed with a 50bps cut in September, with the probability for such action currently resting at around 35%, and the total basis points worth of reductions by December at around 103.

Therefore, data pointing to further cooling of the labor market and more softness in inflation could encourage investors to further lower their implied rate path, something which is likely to exert more pressure on Treasury yields and the US dollar.

Data pointing to further cooling of the labor market and more softness in inflation could encourage investors to further lower their implied rate path

Yen Carry Trade not the favourite game in town

The currencies taking the most advantage of the dollar’s slide were the risk-linked aussie, kiwi, and loonie, as well as the British pound. BoE Governor Bailey’s message that they are not in a rush to cut interest rates again soon is also adding fuel to the pound’s engines.

Yet, the yen is not the victim it used to be during risk-on days. It managed to gain some ground yesterday, implying that investors remain hesitant to take one last ride with the previously overcrowded carry trade.

The yen is not the victim it used to be during risk-on days

Although it is on the back foot today, hawkish remarks by BoJ policymakers are unlikely to allow massive selling. Following Governor Ueda on Friday, Deputy Governor Himino said today that they would continue to raise interest rates if inflation stayed on course. This allowed traders to continue pencilling in a strong 72% chance of another 10bps hike by the BoJ this year.

Equity traders lock gaze on Nvidia

All three of Wall Street’s main indices closed yesterday’s session in the green. With recession fears abating, equity traders are cheering again for lower interest rates in the months to come.

The gains were cautious though, as today, Nvidia is reporting its earnings after the closing bell. Nvidia’s results follow recent concerns about spending increases by other major players in the race to conquer the AI world, and thus, attention may be bigger than usual.

Gains were cautious though, as today, Nvidia is reporting earnings after the closing bell

Indeed, options pricing suggests that traders anticipate larger-than-usual post-earnings moves, which means that the broader market may also experience increased volatility as Nvidia accounts for more than a third of the S&P 500’s gains this year.

Oil slips on consumption worries

Oil prices have rebounded strongly lately on fears about potential supply losses from Libya, as well as increasing tensions in the Middle East. That said, a three-day streak of gains ended yesterday due to concerns about lower refinery profit margins after data showed that global consumption growth has been lower than previously estimated this year.

Yet, the ongoing conflict between Israel and Hamas and the risk of more than 1 million barrels per day of production being shut in Libya amid a political dispute, suggest that any setbacks in oil prices are likely to stay limited and short-lived.

Any setbacks in oil prices are likely to stay limited and short-lived

Source by: XM Global